Tesla Motors 2015 03 31.pdf

Vista previa de texto

4. SLOWING ECONOMIC GROWTH IN DEVELOPED COUNTRIES – A number of developed countries, especially those in the

EU, are expected to face a protracted economic slowdown, looking forward. This would lead to declining wealth and

purchasing power in those regions, in turn leading to a decline in the growth of the car markets there.

5. IMPROVEMENT OF PUBLIC TRANSIT SYSTEMS – A number of countries, such as Switzerland and Singapore, have top

quality public transit systems. Countries such as these aim to discourage the use of cars as the primary mode of

transport among residents in order to reduce traffic and emissions. As public transit systems in other countries

improve as well, dependence on cars will decline, and this will have an impact on the growth of the global passenger

car market.

6. DISRUPTION OF THE TRANSPORTATION INDUSTRY – Newer technologies, like app-based cab services such as Uber and

Lyft, have made many parts of the cities, which were previously not accessible, accessible to users. Over long enough

distances, the cost of using Uber drops below the cost of owning a car. The rise of such technologies might convince

consumers to forego wanting to own a car. Self-driving cars might change the concept of ownership of a car. A selfdriving car does not require a driver, so once it drops a passenger it does need to stay there and can drop another

passenger. This aspect might change the concept of property in relation to cars. People might begin to think of

transportation as a public utility as opposed to a private one. This would result in fewer cars sold.

Sources for historical data and explanations can be found on the Trefis.com website (link)

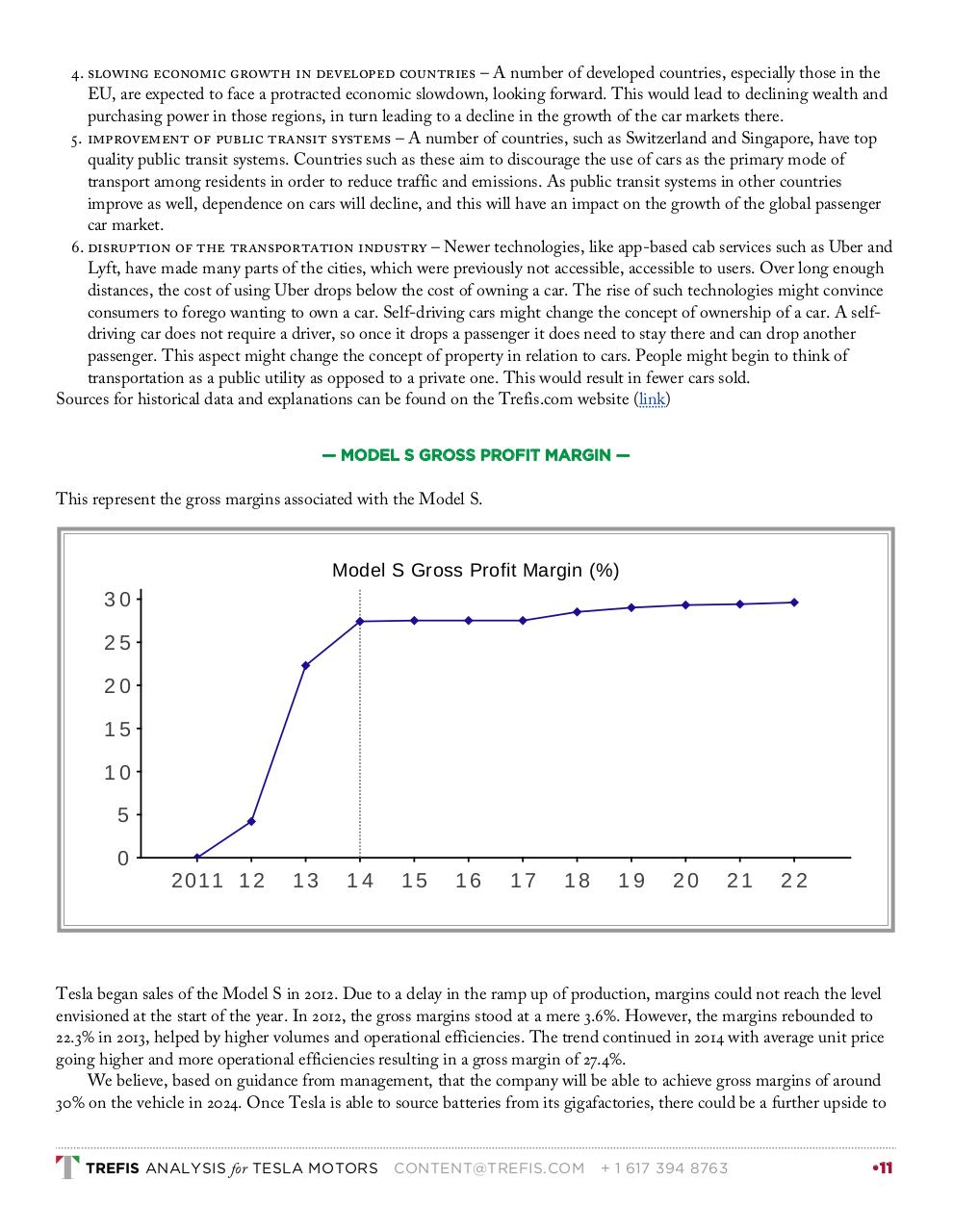

— MODEL S GROSS PROFIT MARGIN —

This represent the gross margins associated with the Model S.

Model S Gross Profit Margin (%)

30

25

20

15

10

5

0

2011 1 2

13

14

15

16

17

18

19

20

21

22

Tesla began sales of the Model S in 2012. Due to a delay in the ramp up of production, margins could not reach the level

envisioned at the start of the year. In 2012, the gross margins stood at a mere 3.6%. However, the margins rebounded to

22.3% in 2013, helped by higher volumes and operational efficiencies. The trend continued in 2014 with average unit price

going higher and more operational efficiencies resulting in a gross margin of 27.4%.

We believe, based on guidance from management, that the company will be able to achieve gross margins of around

30% on the vehicle in 2024. Once Tesla is able to source batteries from its gigafactories, there could be a further upside to

TREFIS ANALYSIS for TESLA MOTORS

CONTENT@TREFIS.COM

+ 1 617 394 8763

•11